Key Takeaways

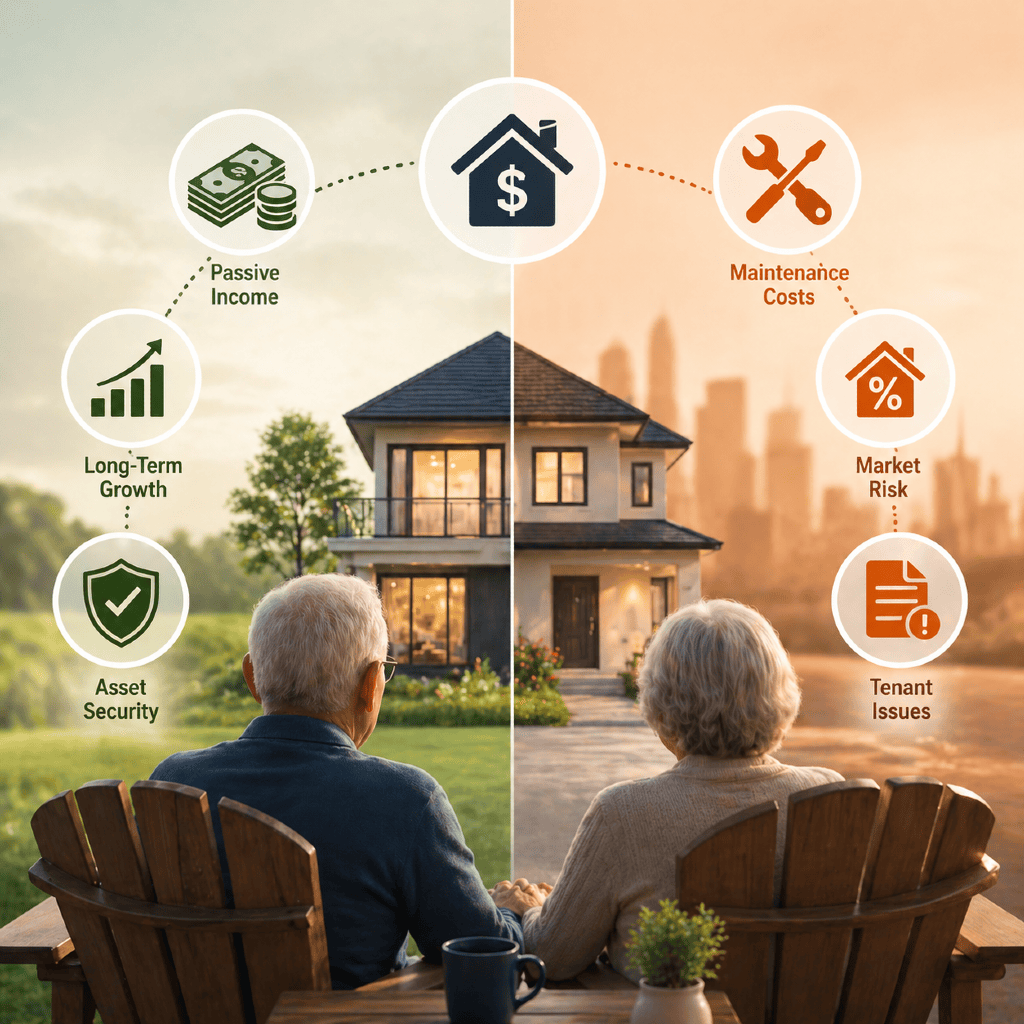

- Real estate income can enhance diversification and provide inflation-resistant cash flow for retirement.

- Potential drawbacks include liquidity challenges, market risks, and ongoing management responsibilities.

Real estate income strategies have become an integral part of conversations around retirement planning. As you look for ways to support your lifestyle in retirement, understanding the ins and outs of real estate income—its types, benefits, and challenges—can help clarify if these approaches align with your long-term goals.

What Are Real Estate Income Strategies?

Definition and Key Concepts

Real estate income strategies refer to ways of generating recurring cash flow from properties. Rather than focusing solely on property appreciation, these strategies emphasize earning income through ownership or investment in real estate assets. Income can be generated from various arrangements, such as collecting rent, leasing commercial spaces, or participating in joint property ventures. This approach is rooted in using real estate as a source of predictable, periodic payments to help meet ongoing retirement needs.

Common Types Used in Retirement Planning

Several real estate strategies are frequently considered in retirement contexts:

- Rental Properties: Buying residential or commercial properties to lease out, earning rental payments.

- Real Estate Investment Trusts (REITs): Investing in companies that own, operate, or finance income-producing properties, typically offering exposure to real estate markets without direct ownership.

- Real Estate Partnerships: Engaging in joint ventures or group investments, pooling resources to acquire and manage property.

Each of these options presents different levels of involvement, risk, and income potential. They are generally evaluated alongside other retirement income resources.

How Do Real Estate Strategies Work for Retirement?

Potential Retirement Income Paths

In the context of retirement, real estate can deliver income in two primary ways:

- Direct Rental Income: Retirees owning property may receive regular rental payments. This can provide relatively steady cash flow, supplementing other retirement income sources.

- Passive Investment Returns: Through vehicles like real estate trusts or partnerships, you may earn distributions or dividends based on property performance, without hands-on management.

These paths can develop into reliable streams, particularly when incorporated thoughtfully into an overall retirement plan.

Core Considerations for Retirees

When integrating real estate into your strategy, several core factors stand out:

- Risk Exposure: Real estate, like any investment, carries market and tenant risks.

- Level of Involvement: Direct ownership demands more time and attention than passive investment structures.

- Income Reliability: Vacancy periods or market downturns can impact predictable earnings.

Understanding these considerations can help you determine if, and how, real estate can support your retirement objectives.

What Are the Pros of Real Estate Income?

Potential for Diversification

Adding real estate to your retirement portfolio introduces an asset class that often behaves differently than stocks or bonds. This diversification can reduce overall portfolio risk since real estate values and incomes may not always move in sync with other investments. For many people, owning income-generating property helps balance market fluctuations and smooth out retirement income.

Income Stream Possibilities

Real estate can serve as a source of ongoing income. Rental payments, for example, may continue monthly or quarterly, supporting recurring expenses in retirement. Passive investments, such as those in real estate trusts, generally pay distributions that can add to other retirement income resources. These options offer an alternative, beyond traditional income sources, to help meet spending needs.

Inflation Protection Aspects

One unique aspect of real estate is its potential to offer some protection against inflation. As the general cost of living rises, property values and rental rates often adjust upward over time. This dynamic can allow real estate income to keep pace with, or even outpace, increases in everyday expenses, helping preserve your purchasing power throughout retirement.

What Are the Cons of Real Estate Income?

Liquidity and Maintenance Challenges

Unlike more easily traded assets, real estate is generally considered illiquid. Selling property or exiting an investment may require significant time and effort, which can pose challenges if you need swift access to cash. Additionally, direct property ownership brings ongoing expenses—maintenance, repairs, taxes, and insurance—that must be managed and budgeted for throughout retirement.

Market and Valuation Risks

Real estate values can fluctuate, sometimes dramatically, due to changes in market demand, economic cycles, or shifts in the local environment. Market downturns or oversupply can affect both the value of the property and the stability of rental income. These risks are important to weigh, especially if you are counting on property income for essential retirement needs.

Management Responsibilities

Owning and managing real estate can entail substantial hands-on work—finding and vetting tenants, responding to maintenance requests, handling legal requirements, and overseeing property performance. For retirees seeking passive income and less day-to-day stress, this can be a significant drawback. While some options, like real estate trusts, mitigate direct management demands, understanding your willingness to manage (or outsource) these tasks is essential.

How Do Real Estate and Traditional Retirement Strategies Compare?

Income Reliability

Traditional retirement income sources (such as retirement accounts or Social Security) are generally viewed as more predictable, with established distribution schedules. In contrast, real estate income may vary due to vacancy periods, tenant turnover, or market influences. Retirees considering real estate as a substantial income source should plan for occasional disruptions or periods of lower cash flow.

Risk Profiles

Real estate carries its own set of risks, including those related to property valuation, tenant reliability, and broader market trends. This risk profile is distinct from traditional sources, which tend to be regulated, insured, or backed by broader financial systems. Understanding these differences helps clarify how real estate fits within your overall portfolio.

Complexity and Oversight Needs

Managing retirement income from real estate can be more complex than other methods due to oversight requirements, legal compliance, and administrative tasks. Whether direct or indirect, real estate investments often come with additional decisions about property management, legal structures, and tax considerations. These added layers may not appeal to every retiree, particularly those favoring simplicity.

Is Real Estate Income Right for Every Retiree?

Assessing Risk Tolerance

You should carefully evaluate your personal risk tolerance when considering real estate income strategies. Those comfortable with some degree of market volatility and hands-on management may find these approaches suitable. On the other hand, individuals seeking stable, predictable income without hands-on demands might consider other retirement income solutions a better fit.

Personal Circumstances to Consider

Factors such as existing assets, health, location, skills, and time available for active management all contribute to the suitability of real estate strategies. It is important to assess your situation honestly, recognizing how much involvement and risk you are prepared to accept throughout retirement.

Long-Term Planning Implications

Adding real estate to your income mix means thinking through the long-term impacts: future cash flow needs, property disposition planning, and potential legacy or estate considerations. Being realistic about ongoing management tasks, as well as planning for unforeseen circumstances, helps create a more confident retirement roadmap.