Key Takeaways

- Retirement emergency preparedness goes beyond health care and savings; understanding coverage and flexible planning is essential.

- Building resilience requires regular review of plans, up-to-date documentation, and staying informed about available community resources.

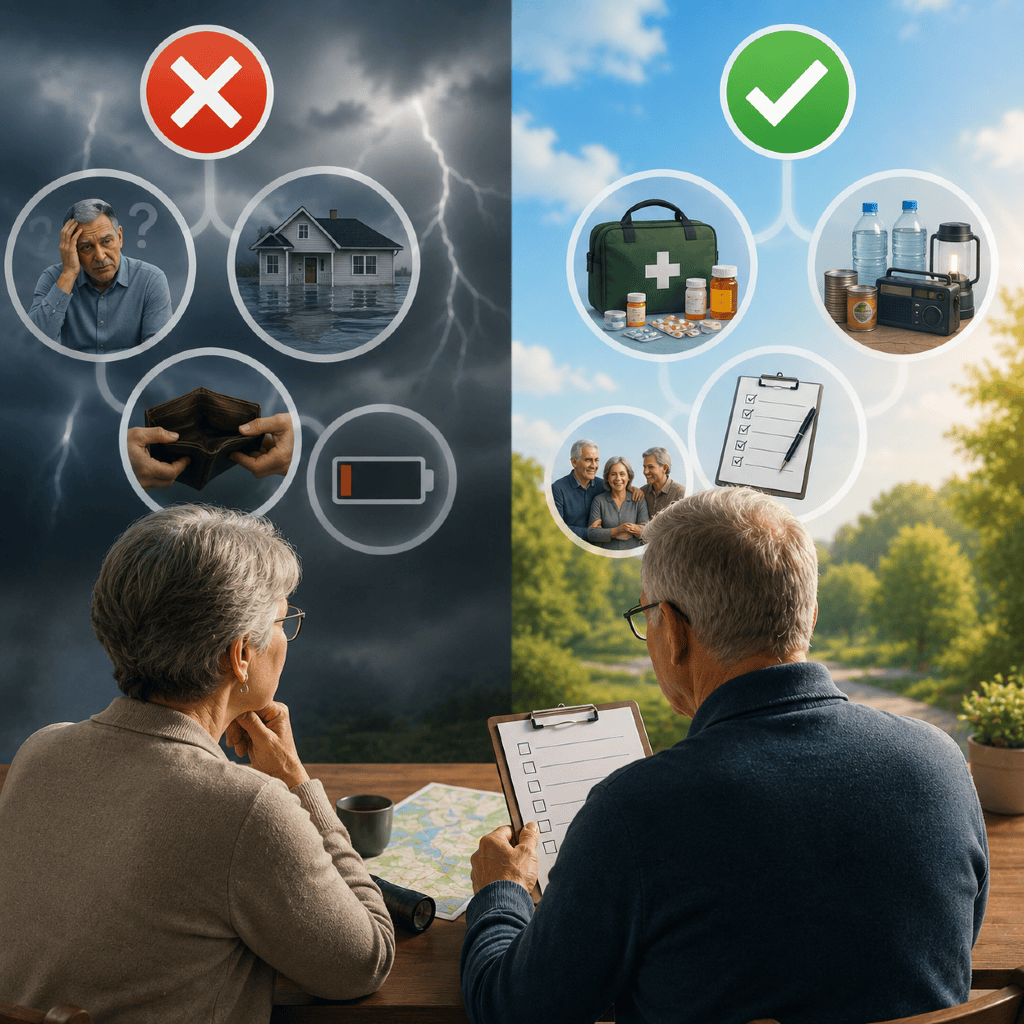

Most retirees feel prepared for the future—until an unexpected emergency arises. Misconceptions about retirement readiness remain common, yet understanding both the risks and the facts allows you to approach your retirement years with confidence and clarity. Let’s explore what true emergency preparedness for seniors involves, separating myth from fact and laying out practical steps to stay resilient.

What Is Emergency Preparedness in Retirement?

Defining key retirement preparedness concepts

Emergency preparedness in retirement is the process of anticipating, planning for, and managing unexpected situations that could threaten your health, finances, or lifestyle during retirement. This is more than simply having enough savings or insurance; it means having clear plans, up-to-date information, and strategies in place to handle a variety of possible disruptions. Effective retirement preparedness focuses on adaptability, awareness, and proactive organization—ensuring you are ready not only for everyday decisions, but also for life’s unexpected turns.

Types of emergencies retirees may face

As a retiree, you may encounter a wide range of emergencies, each with its own considerations:

- Health incidents such as sudden illness, injury, or the need for urgent medical care.

- Natural disasters like storms, floods, wildfires, or other regional crises.

- Financial disruptions including market volatility, fraud attempts, or unplanned expenses.

- Household emergencies such as power outages or home safety issues.

- Personal or family crises where loved ones may depend on your help or decision-making.

Recognizing the scope of possible emergencies is the first step toward comprehensive preparedness.

Why Does Emergency Planning Matter for Seniors?

Risks unique to retirees

In retirement, your circumstances can expose you to unique risks. You may have fixed or limited income sources, changes in health status, increased vulnerability to scams, or a reduced network of close-by family support. Emergency planning helps address these challenges by preparing you for scenarios that can disproportionately impact seniors, such as extended hospital stays, mobility changes, or mandatory evacuations in a local disaster.

Potential impact on retirement security

A well-structured retirement plan can be quickly disrupted by emergencies. Out-of-pocket expenses for care, costs from disaster recovery, or the need to support family members can draw down your resources faster than anticipated. Without an adaptable plan in place, you risk jeopardizing your long-term financial security, and may encounter barriers to accessing necessary services or benefits when timing is critical.

What Are Common Myths About Retirement Readiness?

Myth: Medicare covers all emergencies

A prevalent belief is that Medicare will provide comprehensive coverage for all medical emergencies. While Medicare is a foundational health program for retirees, it is important to understand its scope and limitations. Not all emergency treatments, long-term care services, or follow-up needs may be fully covered, and you will generally be responsible for certain deductibles and co-payments. Additional private coverage or careful saving may be required to bridge these gaps.

Myth: Social Security will handle every need

Social Security is designed to provide a base level of income, not to cover all living expenses or emergency costs. Relying solely on Social Security may leave you financially exposed during a crisis. For example, it does not adjust to sudden expenses resulting from a natural disaster or unplanned medical treatments, making it essential to incorporate other income sources or flexible funds into your planning.

Myth: A savings plan alone is enough

While a robust savings strategy is crucial, emergencies often test more than just your bank account. Being truly prepared means organizing your important documents, knowing how to access additional support, building communication plans with loved ones, and staying informed about local resources—all of which work alongside your savings to provide strong protection.

What Are the Facts on Emergency Preparedness?

Understanding health coverage in retirement

Medicare provides essential coverage, but there are notable limitations. You should review what is and isn’t included, explore the role of supplemental or private insurance, and understand the approval process for different types of care. Building familiarity with the healthcare system in retirement empowers you to act confidently when urgent decisions are needed.

Contingency planning with retirement income sources

Relying on more than one source of retirement income adds flexibility when emergencies strike. This could involve pension benefits, part-time work, structured withdrawals from retirement savings, or other streams such as annuity payouts. Diversifying your sources ensures you can better weather temporary setbacks without risking your core financial security.

Maintaining essential documents and plans

Readiness also means having key documents organized and accessible. These may include a current will, health care directives, durable power of attorney, financial account information, and insurance cards. Keep physical and digital copies in secure but easy-to-reach locations, and share details about their location with trusted individuals.

How Can Seniors Build Emergency Resilience?

Creating a communication plan

Effective emergency prep isn’t just about finances—it’s also about ensuring clear communication. Designate contacts who should be informed during a crisis, compile a list of relevant phone numbers, and discuss specific preferences or contingency steps ahead of time. Practice these communications, so everyone involved knows their role.

Reviewing and updating household documents

Schedule regular intervals to review your documents and plans. Life changes—such as moving, health status shifts, or changes in family structure—can all necessitate updates. Make sure information on household utilities, medical needs, and local support contacts are kept current.

Staying connected to local resources

Local agencies, senior centers, and community organizations often provide resources, support, and alerts relevant to emergencies. Staying informed means subscribing to community updates, joining local networks, and learning where to access services such as shelters, transportation, or food assistance should an emergency arise.

How Do Retirement Preparedness Needs Evolve Over Time?

Ongoing adjustments with age and health changes

Your needs are likely to shift throughout retirement. As your health, mobility, or social connections change, revisit your emergency plans to ensure they continue to align with your reality. Consider how evolving medical needs might affect your response strategies, or whether new types of community support are relevant as you age.

Reviewing plans after major life events

Major events such as the death of a spouse, relocation, changes in income, or the birth of grandchildren can all impact your preparedness strategy. After each significant change, pause to review your contingency plans, update lists of emergency contacts, and assess whether your current coverage and resources fit your needs.