Key Takeaways

- IRMAA surcharges raise Medicare premiums for higher-income individuals, impacting long-term retirement expenses.

- Understanding qualification, calculation, and appeal processes can help you manage and anticipate IRMAA-related costs.

If you’re approaching retirement, you may find that healthcare costs fluctuate based on a little-known factor called IRMAA. This article will help you understand what IRMAA is, how it might affect your Medicare premiums, and how you can proactively plan for these surcharges as you manage your retirement expenses.

What Is IRMAA?

Origin and purpose of IRMAA

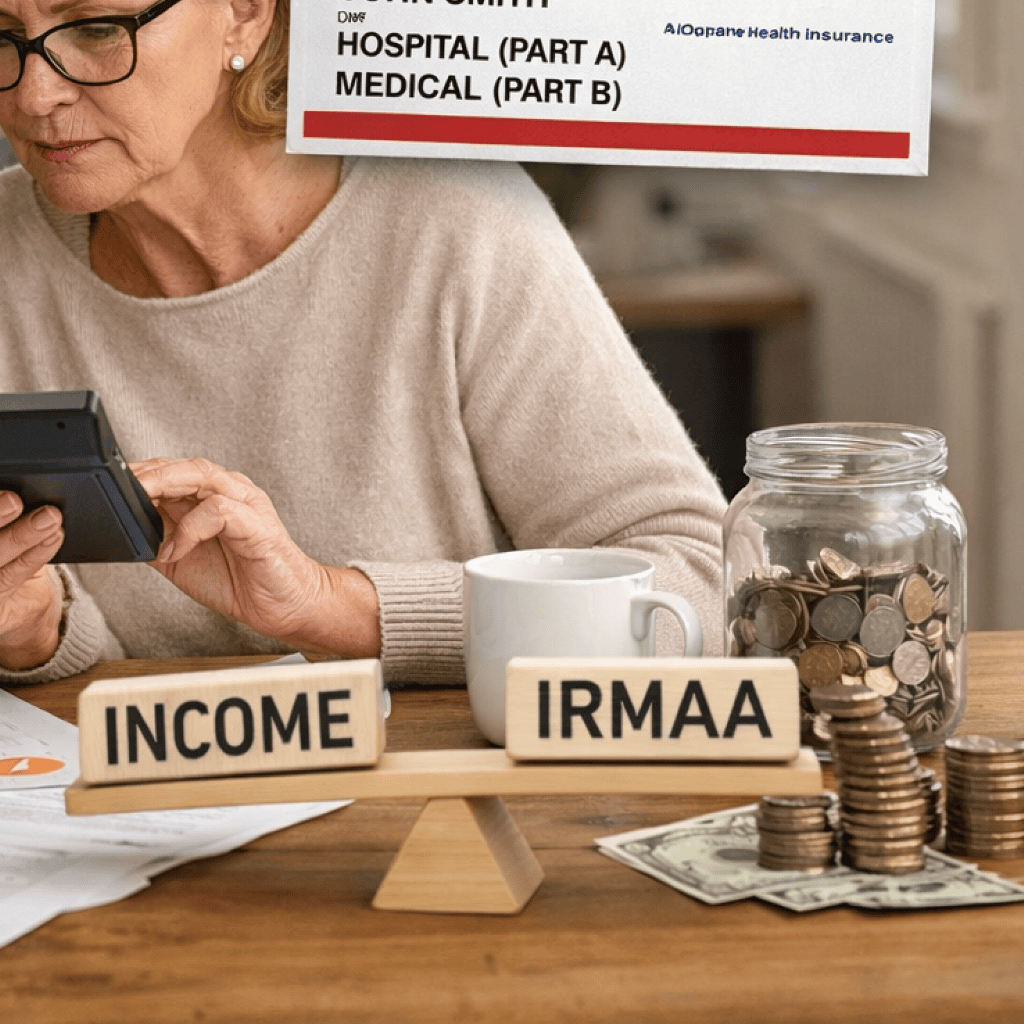

The Income-Related Monthly Adjustment Amount, or IRMAA, is an additional charge affecting some people enrolled in Medicare. IRMAA was established to help ensure that Medicare remains funded by requiring those with higher incomes to contribute a bit more toward their healthcare coverage. The concept emerged in the early 2000s as Medicare sought long-term sustainability by adjusting premiums based on income levels. In practice, IRMAA represents a tiered system of surcharges, meaning those with higher reported incomes pay more for certain parts of Medicare.

Who is affected by IRMAA

IRMAA applies to individuals and households whose income exceeds specific thresholds, which are revisited annually by Medicare policy officials. If your reported income—based on a look-back period—falls above certain brackets, you’ll pay the surcharge in addition to the standard Part B and, in many cases, Part D premiums. The goal is not to penalize retirees, but to reflect capacity to contribute more as retirement income plans shift.

Why Does IRMAA Influence Medicare Costs?

Medicare Parts impacted by IRMAA

Not all areas of Medicare are touched by IRMAA. Mainly, IRMAA applies to two key segments:

- Medicare Part B (outpatient and doctor visits)

- Medicare Part D (prescription drug coverage) Your standard premium for each part serves as the base.

If you’re subject to IRMAA, an additional amount is added on top of these premiums, resulting in a higher monthly healthcare expense.

How IRMAA is determined

IRMAA is calculated using your Modified Adjusted Gross Income (MAGI) from two years prior. For example, your 2026 surcharges will be based on your 2024 income tax return. The Social Security Administration (SSA) reviews your IRS-reported income to determine if an adjustment applies. The process is data-driven and relies on well-defined income categories.

How Are IRMAA Surcharges Calculated?

Income brackets and look-back periods

IRMAA isn’t a flat surcharge—it’s based on a sliding scale. The SSA organizes income into brackets, with each successive level resulting in a higher surcharge. The look-back period is key: SSA examines your tax filing from two calendar years ago to see which bracket applies. These brackets are reviewed annually and can change based on policy updates and national economic factors.

The calculation uses your MAGI, which includes both your adjusted gross income (AGI) and some tax-exempt interest. If you cross a given threshold, your premium is increased according to the bracket your income falls into. This means unforeseen changes in income can potentially impact future healthcare costs.

Life events that can change IRMAA

Life isn’t static, and neither is your income. Recognizing this, Medicare provides ways to account for specific life events that could significantly lower your current income compared to two years ago. Common qualifying events include retirement, divorce, death of a spouse, marriage, or significant loss of income-producing property. If you experience such an event, you may request a review and potentially receive a lower IRMAA assessment.

What Is the Impact of IRMAA on Retirement?

Effect on retirement expenses

For those affected, IRMAA can noticeably increase monthly retirement expenses. Since healthcare often becomes a larger share of the budget as you age, understanding how IRMAA works is critical to getting an accurate picture of your future costs. Even if you only exceed the lowest IRMAA bracket, the increase in premiums could add up over the course of many years in retirement.

Budgeting considerations for retirees

It’s essential to account for the possibility of IRMAA when crafting your retirement budget—particularly if you anticipate higher income from Social Security, pensions, taxable investments, or required minimum distributions. Planning ahead can help smooth out potentially unexpected bumps in your monthly healthcare bill. Regularly reviewing your overall income strategy can keep you informed and prepared for changing premium rates.

Can You Appeal an IRMAA Surcharge?

Common reasons for appeal

If you disagree with the IRMAA surcharge, you aren’t alone—and there are established reasons for appealing. The most frequent triggers for a successful IRMAA appeal are major life-changing events that reduce your income, such as retirement, loss of a spouse, divorce, or an income-reducing event like a business wind-down. The SSA considers these situations valid grounds for review.

Appeal process overview

If you want to challenge your IRMAA determination, start by submitting a formal request for reconsideration through the SSA. You’ll need to provide documentation of your life-changing event and evidence of your current income. The process involves completing the required forms and, in some cases, providing follow-up details. If your appeal is approved, your IRMAA may be reduced or eliminated for future premiums. Staying organized and providing clear evidence are key steps in making your case.

Frequently Asked Questions About IRMAA

How often is IRMAA reviewed?

IRMAA is reviewed annually by the SSA, using your tax information from two years prior. Your surcharge can change each year if your reported income changes.

What income counts toward IRMAA?

The primary measure is your Modified Adjusted Gross Income (MAGI), which typically includes taxable income, Social Security, and certain other sources, including tax-exempt interest.

Does IRMAA apply to all Medicare plans?

IRMAA only applies to Medicare Part B and Part D. Medicare Part A is generally not affected by IRMAA surcharges.

Steps to Manage IRMAA in Retirement

Reviewing your income sources

Periodically reviewing all possible sources of retirement income—including Social Security, pensions, annuities, investment withdrawals, and part-time work—can help you understand your likelihood of surpassing IRMAA thresholds. Adjusting when and how you draw from these sources may help limit or manage your exposure.

Staying aware of policy changes

Medicare policies and income brackets can shift over time. Keeping up with policy updates ensures you’re budgeting with the most current information, potentially avoiding surprises. Educational resources and official updates are useful for maintaining awareness.

Where Can You Find More Information?

Official Medicare resources

The official Medicare website and the Social Security Administration website are primary sources of the latest IRMAA standards, consumption guidelines, tables, and appeal forms. These resources are updated regularly to reflect any changes in IRMAA policy or premium structures.

Educational retirement planning guides

You can expand your understanding of IRMAA with retirement guides from well-known nonprofit retirement and aging organizations. These guides provide context, examples, and planning frameworks designed specifically for individuals planning for and living in retirement.