Key Takeaways

- Immediate annuities start payments soon after funding, offering structured income that differs from deferred options.

- It’s essential to evaluate your retirement needs, liquidity, and income sources before considering an immediate annuity.

Are you exploring ways to convert your retirement savings into a steady income stream? An immediate annuity could offer one potential strategy for creating predictable payouts, but it’s important to understand how it works and what to consider in the context of your broader retirement plan. Here’s a clear guide to the basics, processes, and practical considerations around immediate annuities.

What Is an Immediate Annuity?

Overview of Immediate Payouts

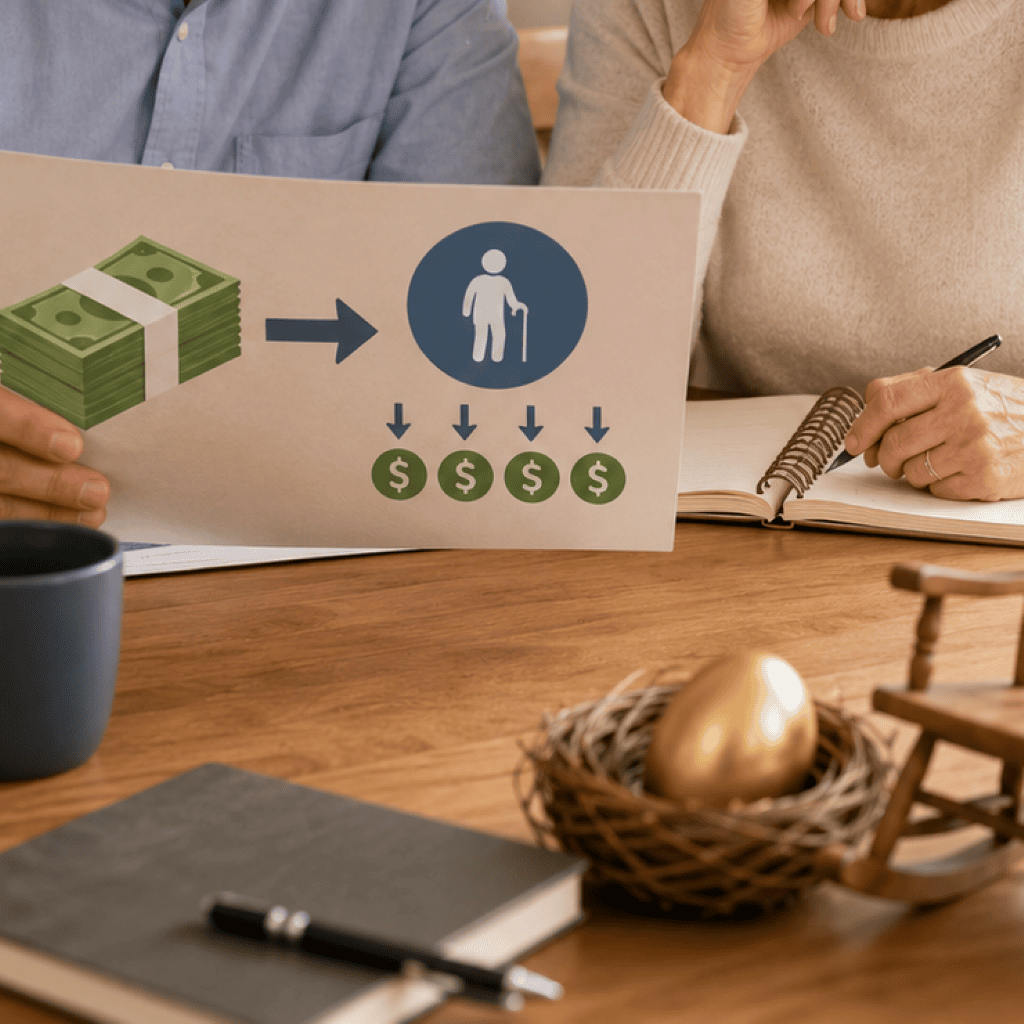

An immediate annuity is a financial arrangement designed to begin paying you regular income shortly after it is funded. In practical terms, this usually means that you make a one-time, lump-sum contribution, and within a short window—often one month—consistent payments start arriving. The intent is to help you transform a portion of your retirement savings into a predictable cash flow.

How It Differs from Deferred Options

Immediate annuities are distinct from deferred annuities. With deferred options, your funds are set aside for growth or accumulation over a period of years before payments start—commonly at a chosen retirement date down the road. Immediate annuities, on the other hand, forgo the waiting period. The focus is on quick conversion from savings to income, aligning with retirees who need income to begin right away.

How Does an Immediate Annuity Work?

Payment Structure Explained

The core idea behind an immediate annuity is regularity and predictability. After you fund the annuity, payments are scheduled at frequent intervals—these could be monthly, quarterly, or annually based on your selection. The payment amount stays consistent for the duration of the chosen payout period. This provides a structure that can be useful for budgeting your retirement expenses.

Typical Funding Approaches

Immediate annuities are typically purchased with a lump sum from your retirement savings. This could include money rolled over from other retirement accounts or proceeds from major financial events, such as selling a business or downsizing your home. Regardless of where the funds originate, the primary condition is that the payout schedule starts almost immediately after funding. This approach contrasts with retirement products designed for gradual or delayed income.

What Are Key Features to Consider?

Payout Frequency Choices

One of the first decisions you’ll face is how often you’d prefer to receive payments. Most immediate annuities offer flexibility here, letting you select from monthly, quarterly, semiannual, or annual disbursements. Opting for monthly income often mirrors the flow of workplace paychecks, which can make household budgeting in retirement easier and more familiar.

Types of Payout Periods

Immediate annuities can structure payments for various timeframes. Common options include income for a set number of years (such as 10 or 20), for your lifetime, or for the joint lifetimes of you and a spouse or partner. Each payout period has advantages and trade-offs related to predictability, longevity risk, and estate planning, so it’s important to align these choices with your goals and circumstances.

Is an Immediate Annuity Right for You?

Assessing Retirement Income Needs

The primary appeal of an immediate annuity is transforming part of your accumulated retirement savings into ongoing income. To determine whether this is a fitting approach, it’s essential to analyze your expected retirement expenses and your projected income from other sources, such as Social Security or pensions. Make sure that your essential needs are covered and that the annuity’s payment structure aligns with your day-to-day cash flow requirements.

Matching Options to Personal Goals

Your retirement goals are unique. Consider whether a structured income stream matches your lifestyle and risk tolerance. If you value the consistency of regular payments and are comfortable with less day-to-day control of those funds, an immediate annuity can play a central role in your income strategy. On the other hand, if flexibility or the ability to access principal is a higher priority, you may want to weigh alternative approaches.

What Are Common Misconceptions?

Understanding Liquidity Trade-Offs

A widely held belief is that an immediate annuity offers complete flexibility—however, once you transfer funds into the annuity, access to those assets in lump sums is generally limited. This reduced liquidity is a fundamental consideration and makes it important to set aside a cash reserve for emergencies or unexpected expenses before you commit funds.

Clarifying Retirement Flexibility

Another misconception is that income from an immediate annuity can easily adapt to changing life events or rising expenses. In reality, most immediate annuity structures provide a fixed payment amount. While this reliability is an advantage for budgeting, it doesn’t offer direct protection against inflation or significant lifestyle changes. Understanding this can help you blend immediate annuity income with other, more flexible income tools in your retirement plan.

Key Considerations Before You Decide

Evaluating Current Retirement Savings

Before committing to an immediate annuity, take a comprehensive look at your total retirement assets. Make sure that the amount you plan to allocate won’t limit your ability to meet other financial needs, and that you still maintain diversified sources of liquidity and growth if those are part of your broader plan.

Coordinating with Other Income Sources

Immediate annuities are most effective when used alongside other retirement income sources. Consider how your annuity payments will interact with Social Security, retirement plan distributions, or part-time work. Together, these resources form the basis of a stable retirement income, protecting you from relying too heavily on a single approach.

How to Start Learning About Your Choices?

Sources for Retirement Education

If you’re researching immediate annuities, start with trusted educational resources. National retirement associations, consumer finance organizations, and objective online platforms focused on retirement income planning can provide foundational knowledge. Reliable public agencies may also offer online tools and guidances to help demystify your options.

Questions to Research Further

Continue your research by asking: What role do I want fixed income to play in my retirement plan? How will I balance predictability with flexibility? What is the opportunity cost of locking up assets versus other approaches? Investigating these questions thoroughly will help you make informed, confident decisions as you shape your retirement income strategy.