Key Takeaways

- Traditional and Roth IRAs offer distinct tax advantages and rules—understanding these differences is essential for effective retirement planning.

- Flexibility, eligibility, and long-term goals can influence whether a Traditional or Roth IRA is the right fit for you.

As you plan for retirement, understanding the main types of Individual Retirement Accounts (IRAs) can help you prepare for a secure future. This guide will walk you through how Traditional and Roth IRAs work, outline their rules, examine tax benefits, and compare their unique features so you can make informed decisions.

What Is a Traditional IRA?

Definition and purpose

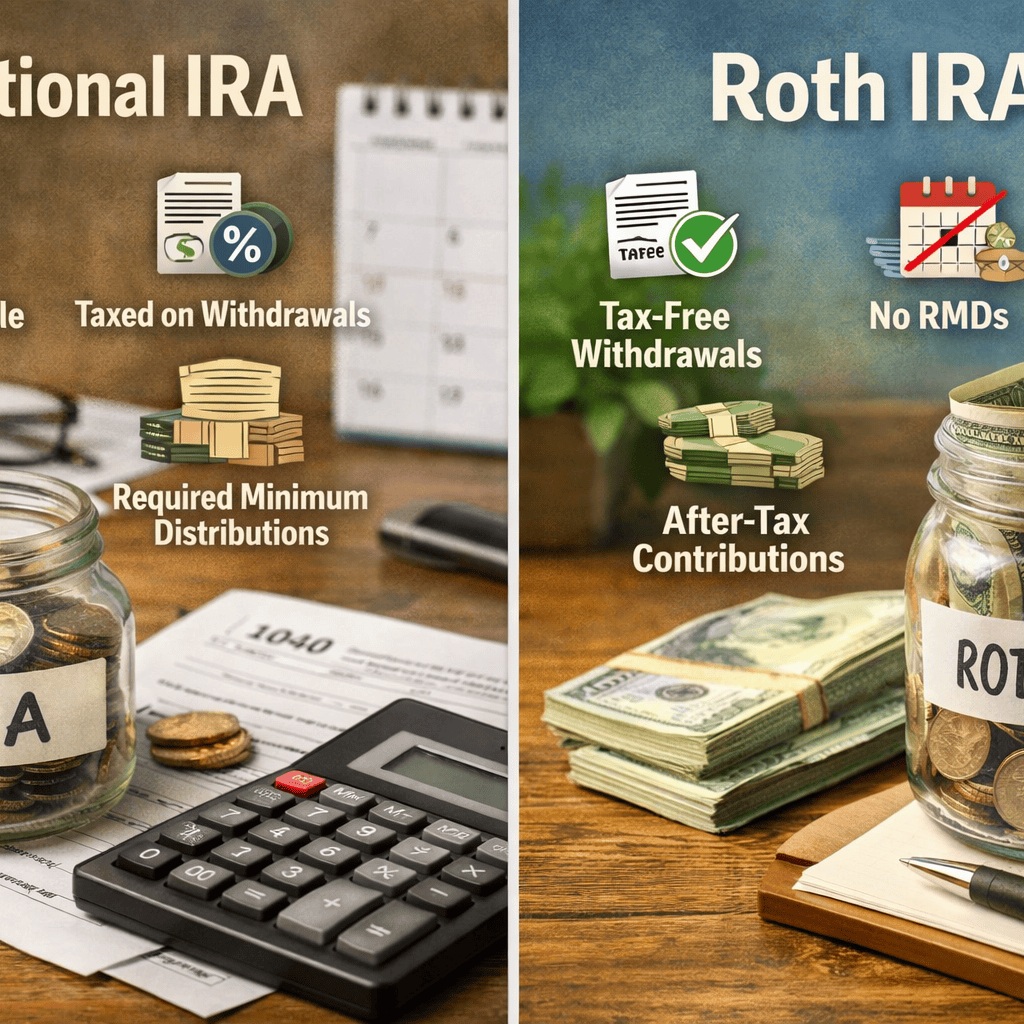

A Traditional IRA is a type of retirement savings account that lets you save for the future while potentially reducing your taxable income in the present. It’s designed to help you build retirement savings on a tax-deferred basis, meaning you might not pay taxes on contributions or earnings until you make withdrawals in retirement.

How contributions work

You can contribute to a Traditional IRA if you have earned income. Contributions may be tax-deductible, which means you could lower your taxable income for the year you make the contribution. However, the amount you can deduct may depend on your income and whether you or your spouse are covered by a workplace retirement plan. The Internal Revenue Service (IRS) sets annual contribution limits, and these limits apply across all your IRAs combined.

Withdrawal guidelines

Withdrawals, also called distributions, are permitted from age 59½ onward without penalty. If you withdraw funds before this age, you’ll generally pay both income taxes and an additional penalty on the amount taken out, unless you qualify for an exception, such as certain medical expenses or a first-time home purchase. At a certain age, you must begin taking required minimum distributions (RMDs), ensuring the government can tax those savings.

How Does a Roth IRA Work?

Roth IRA overview

A Roth IRA is another personal retirement savings account, but its focus is on after-tax contributions. This means you pay taxes on the money before you put it in, and qualified withdrawals in the future may be tax-free. The Roth IRA is popular among those who expect to be in a higher tax bracket during retirement or who want to limit future tax obligations.

Contribution rules

To contribute to a Roth IRA, you need earned income, and your ability to contribute may be limited or phased out based on your income level. Unlike the Traditional IRA, your contributions are not tax-deductible. The same total annual contribution limits apply across both Traditional and Roth IRAs.

Withdrawal and access

One standout feature of the Roth IRA is flexibility: you can withdraw your contributions at any time without taxes or penalties, since you have already paid income taxes on that money. However, investment earnings in your Roth IRA need to stay in the account for at least five years and until you are at least 59½ to be considered qualified and tax-free. Early withdrawals of earnings may trigger taxes and penalties unless an exception applies.

What Are the Key Differences?

Tax treatment of contributions

Traditional IRA contributions may be tax-deductible for the year they are made, reducing your taxable income in the present. Roth IRA contributions are always made with after-tax dollars, offering no deduction upfront.

When taxes are paid

With a Traditional IRA, taxes are deferred until you withdraw funds in retirement. All withdrawals are generally taxable as ordinary income. For Roth IRAs, you pay taxes before adding money to the account, but eligible withdrawals (including earnings if qualified) are not taxed in retirement.

Withdrawal rules compared

Traditional IRAs impose taxes and possible penalties on early withdrawals. Once you reach a certain age, you’re required to take annual distributions. With a Roth IRA, you never have to take RMDs during your lifetime, and you can access your contributions penalty-free at any time. Earnings in a Roth IRA require you to meet specific criteria for tax-free withdrawal.

Which IRA Offers Greater Flexibility?

Accessing funds early

A Roth IRA generally lets you access your contributed funds any time without taxes or penalties, making it more flexible for unexpected expenses. In contrast, a Traditional IRA will typically trigger taxes and possibly penalties if you withdraw before reaching the qualifying age, except for specific exceptions.

Required minimum distributions

Traditional IRAs require you to begin taking minimum distributions by a certain age, whether you need the funds or not. This means you will eventually start paying taxes on your savings. Roth IRAs, however, do not require minimum distributions during your lifetime, giving you more control over your account.

Changing account types

If your needs or situation change, you may be able to convert all or part of a Traditional IRA to a Roth IRA. This is called a Roth conversion. Be aware that when you convert, you’ll typically owe taxes on the amount you move, since you’re shifting pre-tax money into an after-tax account. The rules can be complex, so careful planning is important.

What Should You Consider Before Choosing?

Income and eligibility

Your eligibility to deduct Traditional IRA contributions or contribute to a Roth IRA often depends on your income level and if you’re covered by a workplace plan. Check current IRS guidelines to see what’s allowed for your situation.

Long-term goals

Think about your expected income after retirement and your current tax bracket. If you believe you’ll be in a lower tax bracket in retirement, a Traditional IRA might seem more attractive. If you expect higher income, or want to avoid future required withdrawals, a Roth IRA’s tax-free withdrawals could make more sense.

Tax implications for retirement

Deciding between pre-tax and after-tax contributions could shape your retirement strategy. Some individuals spread their savings across both types to benefit from tax diversity. This approach can help manage taxable income as your needs and tax laws evolve.