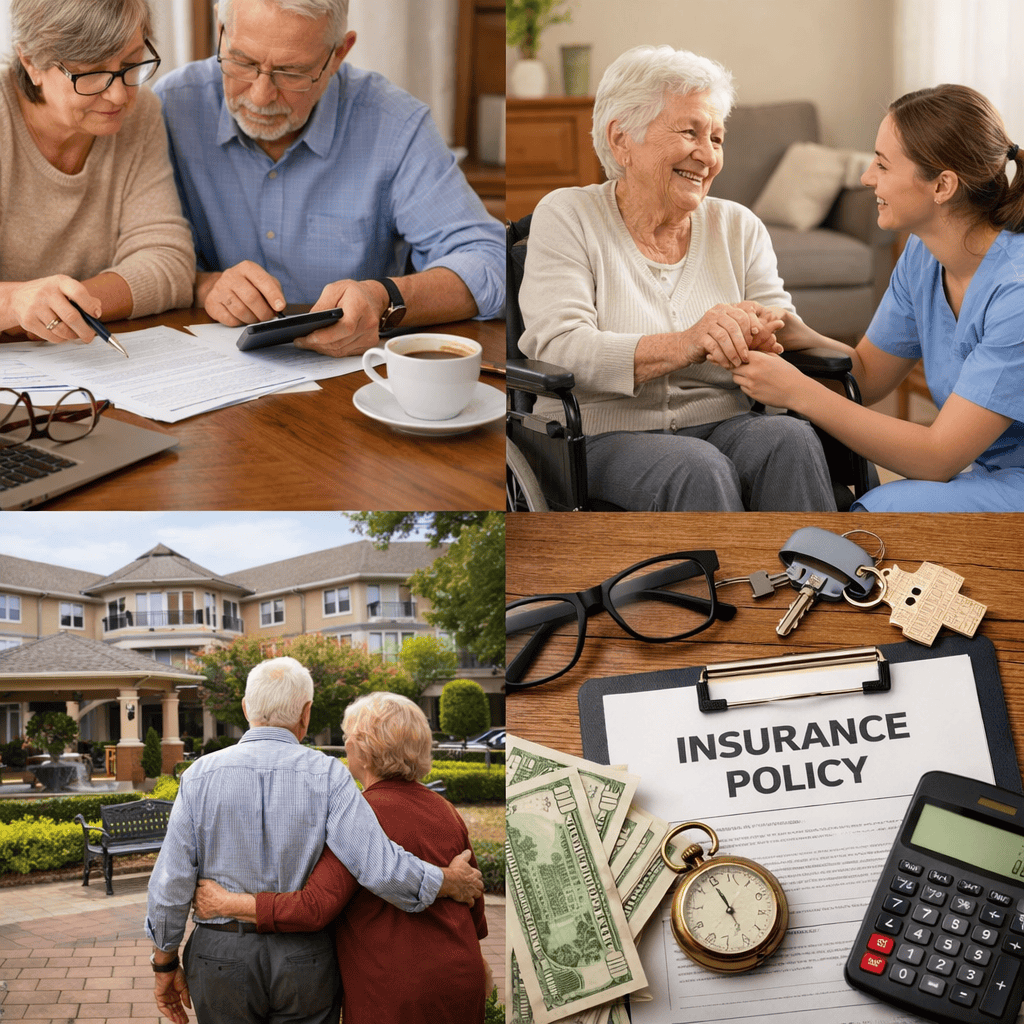

Long-Term Care Insurance Q&A: Coverage, Costs, and Policy Basics for Retirees

Key Takeaways

- Long-term care insurance helps cover services that traditional health plans and Medicare rarely include.

- Your needs, health, and timing all influence whether long-term care insurance could play a role in your retirement strategy.

Are you thinking about how your healthcare needs might change later in life? Long-term care insurance is a unique tool that can help with services most health plans don’t cover. Let’s walk through the basics: what it is, how it works, costs, and key policy features — all tailored for today’s retirees and future planners.

What Is Long-Term Care Insurance?

Definition and basic concept

Long-term care insurance is a policy that helps pay for care you may need if you’re unable to perform everyday tasks on your own due to an illness, injury, or aging. This type of coverage is designed to fill the gaps where standard health insurance or Medicare usually fall short. Rather than paying medical bills, this insurance focuses on custodial care — helping with activities like eating, bathing, dressing, and moving around your home or a care facility.

Who might need this coverage

While anyone could need help with daily activities, long-term care needs are more common as you get older. If you’re approaching retirement or noticing changes in your ability to do everyday tasks, it’s a good time to consider whether this insurance could make sense for you. It’s also valuable if you have a family history of chronic health conditions or want to protect your retirement savings from high care costs.

How Does Coverage Work?

Covered services overview

Long-term care insurance typically covers a range of services not included under health insurance plans or Medicare. These may range from in-home care—like home health aides and personal care assistants—to care provided in assisted living facilities, adult day care centers, and nursing homes. The goal is to support you with daily living activities, whether you need a little help at home or full-time supervision elsewhere.

Types of care included

Most policies are designed to be flexible. Covered types of care can include in-home personal care, help with chores, assistance with mobility, and supervision for memory-related conditions such as Alzheimer’s disease. Facility-based care, like assisted living or nursing homes, can also be covered, depending on your policy terms.

What Costs Should Retirees Expect?

Premiums and payment structures

When you purchase a long-term care insurance policy, you pay a regular premium. The amount and payment frequency will depend on your chosen coverage options, age at purchase, and health status. Premiums are typically set at the start but can go up over time if the insurance company raises rates for an entire group of policyholders.

Factors influencing costs

Your age, health, the benefit amount, and length of coverage all factor into the cost of premiums. Generally, buying earlier in your 50s or early 60s lets you lock in lower initial premiums—though you’ll pay longer over your lifetime. Waiting until later might lead to higher costs or make it harder to qualify if your health has changed. Policy features like inflation protection and shorter elimination (waiting) periods can also influence your overall cost.

Can You Customize Coverage Levels?

Optional benefit features

Most insurance providers offer a range of benefit features you can add to your policy for more tailored protection. These can include inflation adjustments (so benefits keep up with rising care costs), shared coverage for couples, and shorter or longer waiting periods before benefits start paying. You can select benefit amounts and daily or monthly limits that work for your budget and anticipated needs.

Adjustment possibilities

Even after purchase, there may be chances to tweak certain elements of your policy. You might be able to reduce benefits or adjust how long your coverage lasts if your life circumstances or health status change. However, adding more benefits or increasing coverage may require additional underwriting, especially as you age. Carefully review adjustment options before purchasing so you know what’s possible down the line.

When Should You Consider Long-Term Care Insurance?

Typical life stages for review

People often begin looking at long-term care insurance in their mid-50s to early 60s, while they are healthy enough to qualify and premiums are lower. It’s wise to review your options ahead of major retirement milestones or changes in health. Early planning may offer more choices and help you integrate this coverage into your broader retirement income strategy.

Health and family factors

If you have a family history of chronic illness, memory loss, or early-onset health issues, considering coverage sooner can be valuable. Couples may also benefit from planning together, since shared needs can affect policy selection and costs. Even if you’re in good health now, reviewing your choices early means fewer surprises later.

What Are Common Exclusions?

Services not typically covered

Most long-term care policies have exclusions. For instance, they typically do not cover care needed due to self-inflicted injuries, certain mental disorders, or care already covered by other insurance. Pre-existing conditions may not be covered for a waiting period, and services unrelated to assistance with daily living or medical necessity may be excluded.

How exclusions impact decisions

Understanding exclusions helps you set realistic expectations about your coverage. If you have specific needs or conditions, make sure to check whether they will be covered. This also helps you determine if you need to look into supplemental options, other coverage, or health planning strategies.

Does Medicare Cover Long-Term Care Needs?

Medicare’s limits on long-term care

A common misunderstanding is that Medicare provides broad long-term care benefits. Actually, Medicare primarily covers medical needs and provides only limited short-term support for skilled nursing or rehabilitation, often after a hospital stay. Ongoing custodial care—meaning regular help with daily tasks at home or in a facility—is generally not included.

Importance of supplemental options

Because Medicare’s coverage is limited for long-term care, retirees often need to look at other options, such as long-term care insurance or personal savings, to plan for these expenses. Understanding this gap is key so you don’t find yourself unprepared for the potential cost of care in retirement.

What Questions Should Retirees Ask First?

Assessing readiness for coverage

Start by asking yourself how you would handle a need for ongoing daily assistance. Do you have family or other resources to rely on, or do you want the predictability of insurance coverage? Explore your financial situation, current health, and goals for protecting your assets.

Understanding personal circumstances

Everyone’s needs are different. Think about your family medical history, current health, living situation, and personal preferences. By understanding these factors, you can better assess if long-term care insurance, or another solution, makes sense for your retirement plan.

How Do Policy Terms Affect Benefits?

Benefit triggers overview

A “benefit trigger” is the condition that must be met for your policy to start paying benefits. Usually, this means needing help with two or more activities of daily living (ADLs), such as bathing or dressing, or having severe cognitive impairment.

Policy duration and benefit periods

Policies vary in how long they pay benefits. Some offer set periods, such as two, three, or five years, while others offer longer durations. The longer the benefit period and the higher the payment maximum, the more costly the policy usually becomes. Know these terms before you purchase and compare them to your own potential needs.

Is Long-Term Care Insurance Right for Everyone?

Alternative coverage options

Long-term care insurance is just one way to fund care. Alternatives include relying on personal savings, using home equity, or exploring hybrid life insurance solutions. Some may prefer to self-fund care, while others lean toward insurance for added confidence.

Evaluating personal needs

Deciding if long-term care insurance fits your plan depends on your risk tolerance, finances, and family situation. It’s not essential for everyone, but learning about your choices and carefully weighing the pros and cons is a smart step in retirement planning.