Key Takeaways

- Single and joint pensions provide distinct survivor benefits and payout options.

- Personal priorities, health, and household needs are crucial in making pension decisions.

Many retirees are surprised to learn that their pension decision may affect financial security for themselves and their loved ones—understanding your options is an important part of retirement planning. Navigating the choice between single and joint pension options is a valuable exercise to help ensure you and your family are prepared for the years ahead.

What Are Single and Joint Pensions?

Defining single life pension approach

A single life pension, sometimes called a single-life annuity, provides income payments throughout your lifetime but does not extend benefits to another person after your passing. If you select this option, payments will generally stop when you die, and no further benefits are paid to anyone else. This type of pension approach focuses on maximizing income for your lifetime only.

Defining joint and survivor pension options

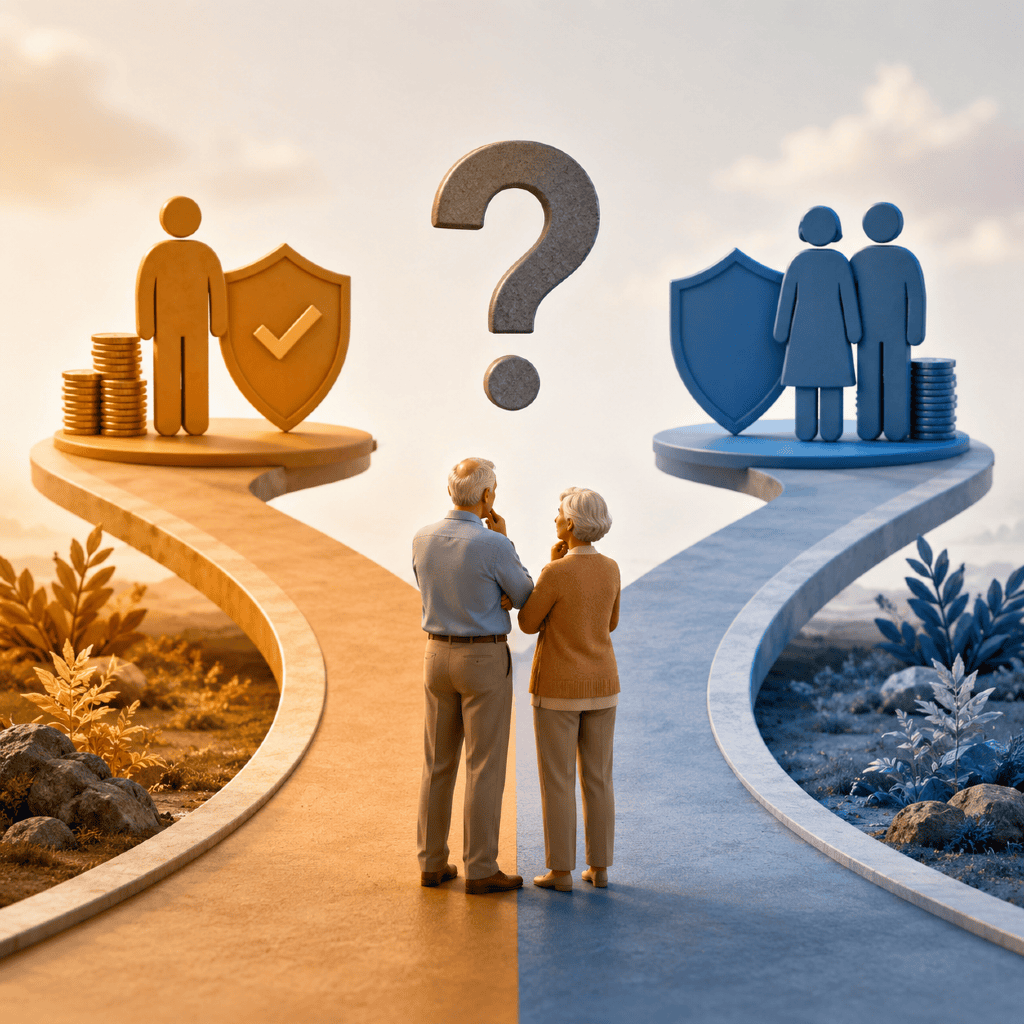

In contrast, a joint and survivor pension is structured so that two lives—typically yours and a spouse or partner’s—are covered. When you pass away, income payments continue for your spouse or designated survivor, usually at a percentage of the original amount. The joint approach is designed for couples or households seeking to ensure that some level of pension income will remain available to a surviving spouse or partner after the pension holder’s death.

How Do These Approaches Differ?

Payout structure overview

The most noticeable difference between single and joint pension options is the payment structure. A single life pension generally offers a higher monthly payout because it is calculated to cover just your life expectancy. A joint and survivor pension, however, usually provides a lower monthly payment, since benefits are likely to be paid over two lifespans. The reduction in payment is essentially the “cost” of ensuring ongoing survivor benefits.

Impact on surviving spouse

For those who are married or partnered, a joint and survivor option helps protect your household’s financial continuity. If you choose a single pension and are the first to pass away, your spouse could lose your pension payment entirely. A joint and survivor pension can help avoid this scenario by providing continued income. It’s important to note, though, that these survivor payments are often (but not always) less than the full amount you received while both spouses were alive.

What Factors Influence Your Choice?

Longevity and health considerations

When evaluating pension options, your health and life expectancy are major considerations. If you are in good health with a family history of longevity, you may want to weigh the long-term advantages of guaranteed survivor income for your household. On the other hand, if you or your spouse have significant health concerns or reduced life expectancy, a single life pension might provide more income during your retirement years, albeit with greater risk for your survivor.

Household finances and needs

The overall financial picture of your household should also influence your decision. If your spouse relies heavily on your pension income, maintaining a joint and survivor option can be critical for ongoing stability. However, if you have multiple income sources, such as Social Security, retirement savings, or other protected benefits, choosing a single life pension may be more appropriate, freeing up income for other goals or contingencies.

Family situation and beneficiaries

Consider your family makeup and intended legacy. Joint pensions are most commonly used by those with spouses or life partners, but some plans allow you to name a non-spouse beneficiary. If you’re single or your spouse will not depend on your pension, a single life option might suit your situation. For those who wish to leave assets to children or others, keep in mind that most pensions do not pass to non-spousal heirs unless you select a specific survivor or guarantee period feature, often at the cost of reduced payments.

Frequently Asked Questions on Pensions

Impact of pension selection on taxes

Your pension selection may impact how your retirement income is taxed, but this is generally influenced by broader income levels, your filing status, and regional tax regulations. The choice between single or joint pension options often does not substantially alter your overall tax liability, but the size and timing of the income stream may affect which tax bracket you and your survivor occupy in retirement. Be sure to review general tax concepts and consider how they may intersect with your unique retirement plan.

Can you change your pension choice later?

In most cases, pension decisions—especially regarding single versus joint structures—are irrevocable after payments begin. Once you start receiving monthly payments, you typically cannot change from one type of payout to another. It’s important to make this decision with care and clarity, evaluating both your immediate and long-term retirement needs upfront.

How to Weigh Your Pension Options

Assessing your personal priorities

Begin by clarifying your financial priorities and retirement goals. Consider what level of income you’ll need, how long you may need it, and the kind of security you want to leave your spouse or partner. Reflect on risk tolerance, comfort with reduced payments for survivor protection, and any other income or savings you can count on. Creating a list of “must-haves” and “nice-to-haves” can help you weigh trade-offs more effectively.

Seeking general retirement planning guidance

While the decision is deeply personal, referring to general principles from retirement planning can help you find direction. Educational resources about retirement income strategies, longevity planning, and spousal protection are widely available. Use these to build knowledge and confidence, so your choice reflects your household’s unique needs and circumstances.

Are There Common Misconceptions?

Assumptions about survivor benefits

One widespread misconception is that all pensions automatically continue to your spouse after you pass away. In reality, only the joint and survivor options provide for a guaranteed benefit to a surviving spouse. If you select a single life pension, payments generally stop when you die. Always review your plan’s details, as the types and percentages of survivor benefits can vary.

Understanding flexibility and limitations

Another misunderstanding is related to the flexibility of pension elections. Pension choices, particularly single or joint payout selection, are generally permanent. Some believe changes can be made after payments start, but most plans restrict alterations once irrevocable decisions are made. Recognizing these limitations will help you set realistic expectations and avoid future regret.

By understanding both the differences and practical considerations of pension options, you place yourself—and your family—on firmer financial footing for retirement. Informed preparation is the best step toward lasting security and peace of mind.