Key Takeaways

- Proper asset allocation helps you manage risk and support retirement income needs.

- Regular portfolio reviews and thoughtful diversification are essential for adapting to life and market changes.

Many retirees report that managing investment risk ranks among their highest concerns. Understanding asset allocation is crucial for building confidence and security as you work toward or live in retirement. In this guide, you’ll explore how to approach asset allocation, assess your own risk comfort, and adapt your portfolio to life’s transitions.

What Is Asset Allocation?

Basic definition and explanation

Asset allocation refers to how you divide your investments among different asset classes, such as stocks, bonds, and cash. The goal is to create a mix that aligns with your financial objectives, time horizon, and comfort with risk. Rather than relying on a single asset’s performance, you spread your investments to balance the potential for returns against risk exposure.

Role in retirement planning

During retirement, asset allocation becomes even more important. Your focus typically shifts from growing wealth to generating sustainable income while preserving what you’ve built. The right allocation can help you weather market fluctuations and smooth your retirement income flow over many years.

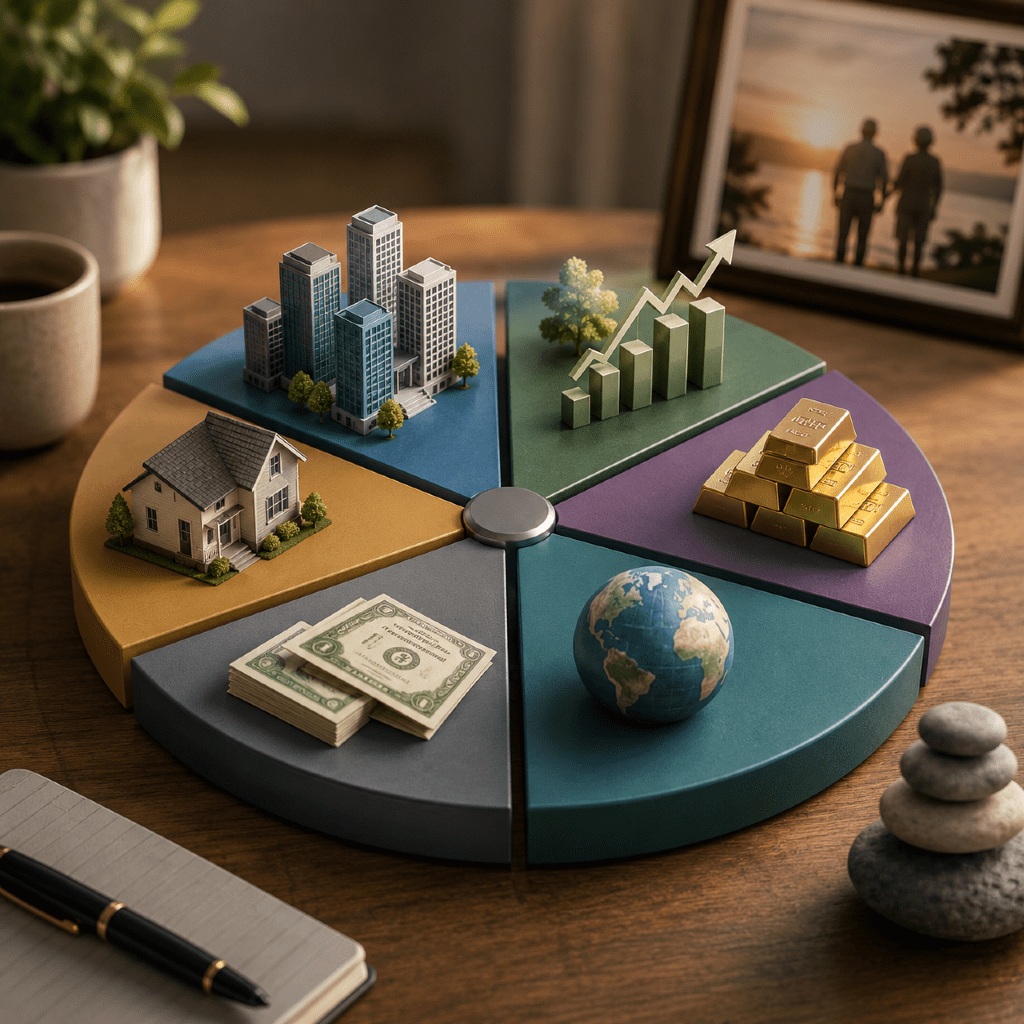

Common types of asset classes

The major asset classes in retirement planning include:

- Stocks (equities): Offer growth potential but higher volatility.

- Bonds (fixed income): Provide income and tend to be less volatile.

- Cash or equivalents: Highly liquid and stable but with limited growth potential.

- Alternative assets: Real estate, commodities, or similar investments can add diversification, though these may carry unique risks and are less common in most traditional retirement portfolios.

Why Does Asset Allocation Matter in Retirement?

Impact on retirement income

Asset allocation directly guides how your portfolio supports retirement income. The right mix helps your savings last and enables you to respond to unexpected expenses. If your allocation is too conservative, you may outpace inflation. Too aggressive, and market downturns could erode your principal faster than planned.

Managing different types of risk

Retirement portfolios face various risks—market risk, inflation risk, longevity risk (outliving your savings), and sequence risk (market losses early in retirement). Strategic allocation spreads these risks. For example, holding both stocks and bonds can reduce the likelihood that one market event disrupts your entire financial plan.

Balancing growth and preservation

Striking the right balance involves keeping enough growth-oriented assets (like stocks) to help beat inflation, while maintaining more stable assets (like bonds) for income and downside protection. You’ll weigh your growth needs against your comfort with market ups and downs.

How Do You Assess Your Risk Tolerance?

Factors influencing risk preferences

Your risk tolerance is influenced by your age, investment experience, financial goals, and emotional comfort with market changes. For example, if you’re further from retirement, you might be able to take on more risk, while those in or near retirement often prefer greater stability.

Changes in risk perspective during retirement

Risk preferences naturally evolve. As you enter retirement or experience life changes (such as health concerns), your ability to withstand losses may decrease. Regularly reevaluating your comfort level ensures your portfolio continues to support your changing needs.

Tools for understanding your comfort level

Various questionnaires and risk assessment tools can help you determine your risk appetite. These often ask how you’d react to hypothetical market losses or gains. Reviewing historical market scenarios, ideally with a financial planner or trusted resource, can also provide perspective.

Key Principles for Balancing Risk and Reward

Diversification across asset classes

Diversification is like building several bridges instead of just one. By investing across asset classes and sectors, you reduce the chance that any single event undermines your financial security. It can also help smooth out portfolio returns over time.

The impact of time horizon

How long you expect your money to last influences allocation decisions. If you anticipate drawing from your portfolio over decades, you might maintain some exposure to growth assets. Conversely, if you need short-term stability, increasing fixed-income allocations may be appropriate.

The importance of regular reviews

Markets change, and so do your circumstances. Reviewing your asset allocation at least once a year—or after major life milestones—helps keep your portfolio aligned with your goals. Regular reviews also help you respond to shifting market trends without overreacting to normal market volatility.

What Are the Main Components of a Retirement Portfolio?

Stocks and equities in retirement

Stocks provide growth potential, which is useful even in retirement for keeping up with inflation. Often, retirees hold a smaller proportion of stocks than younger investors, but enough to provide some long-term growth.

Fixed-income options and considerations

Fixed-income assets—such as government or corporate bonds—offer regular interest payments and can cushion your portfolio during turbulent times. The right mix depends on your income needs, risk profile, and investment timeline.

Alternative and cash asset classes

Alternatives might include real estate or commodities, which sometimes act differently than stocks or bonds. Cash and equivalents (like money market funds or short-term certificates) serve as a safeguard for emergencies and provide immediate liquidity.

How Often Should You Rebalance in Retirement?

Purpose of rebalancing

Rebalancing means restoring your portfolio’s original allocation if market movements lead to drift. For example, if stocks grow significantly, they may exceed your target percentage, potentially exposing you to more risk than intended.

Common rebalancing intervals

Many retirees review and rebalance their portfolios annually or semiannually. Others may choose to rebalance when allocations shift beyond specific thresholds (for instance, 5% off target). The important thing is to rebalance consistently and unemotionally.

Factors affecting rebalancing decisions

Factors such as changing income needs, tax considerations, and transaction costs play a part in your rebalancing strategy. Significant economic or market shifts can also prompt more frequent reviews, especially if your situation or risk tolerance changes.

Common Considerations When Adjusting Allocation

Life events and transitions

Major changes—marriage, divorce, health shifts, or the passing of a partner—can affect how you approach risk and withdrawal needs. Adapting your portfolio to these events ensures continued alignment with your personal goals.

Changing income needs

As your retirement progresses, your income needs may change due to healthcare, housing, or leisure spending. Adjusting your asset allocation can help you accommodate these evolving demands, ensuring continued stability.

Economic and market influences

Inflation rates, interest rate changes, and broader market trends can influence your allocation choices. Staying informed and being willing to adjust your mix help you respond proactively, rather than reactively, to market stress.