Key Takeaways

- Many misunderstandings about QLACs can impact retirement planning decisions.

- Clear knowledge of QLAC rules helps ensure they are appropriately considered among retirement income options.

Qualified Longevity Annuity Contracts (QLACs) are a unique element in retirement planning, yet misunderstandings abound regarding how they work, who can use them, and what they actually provide. A clear grasp of QLACs can help you assess their place in long-term retirement security strategies.

What Is a Qualified Longevity Annuity Contract?

How QLACs Fit into Retirement Planning

A Qualified Longevity Annuity Contract is a specialized retirement tool designed to provide income later in life, often starting well past the traditional retirement age. Their main role is to offer a steady source of income beginning as late as age 85, helping to provide financial security against the risk of outliving other retirement savings. QLACs can alleviate the fear of longevity risk—the possibility of exhausting your regular retirement assets while you still need income.

Basic Features of QLACs

QLACs are a form of deferred income annuity specifically structured for use within certain tax-qualified retirement accounts, such as traditional IRAs and 401(k) plans. The defining feature is their ability to defer the start of required minimum distributions (RMDs) on the portion of retirement assets allocated to the contract, under certain guidelines. Payments from a QLAC cannot begin later than a specified maximum age, and there are federal rules governing the contribution amount and timing.

Who Can Use QLACs?

Eligibility Criteria Overview

Not everyone can utilize a QLAC. Eligibility is restricted to individuals with assets in qualifying retirement plans like traditional IRAs or eligible workplace plans. There are contribution limits, and these limits are monitored each year by the Internal Revenue Service. QLACs are not available within Roth IRAs, and rules regarding other account types must be carefully reviewed to ensure compliance.

How Age and Account Types Factor In

The contract must be purchased using funds from eligible accounts, and there are age-related stipulations. Generally, QLACs are structured to begin distributing income no later than the required beginning date for distributions under applicable IRS rules, but they must start by a certain maximum age defined by regulation. Always check the most current IRS guidance for up-to-date requirements regarding age and account eligibility.

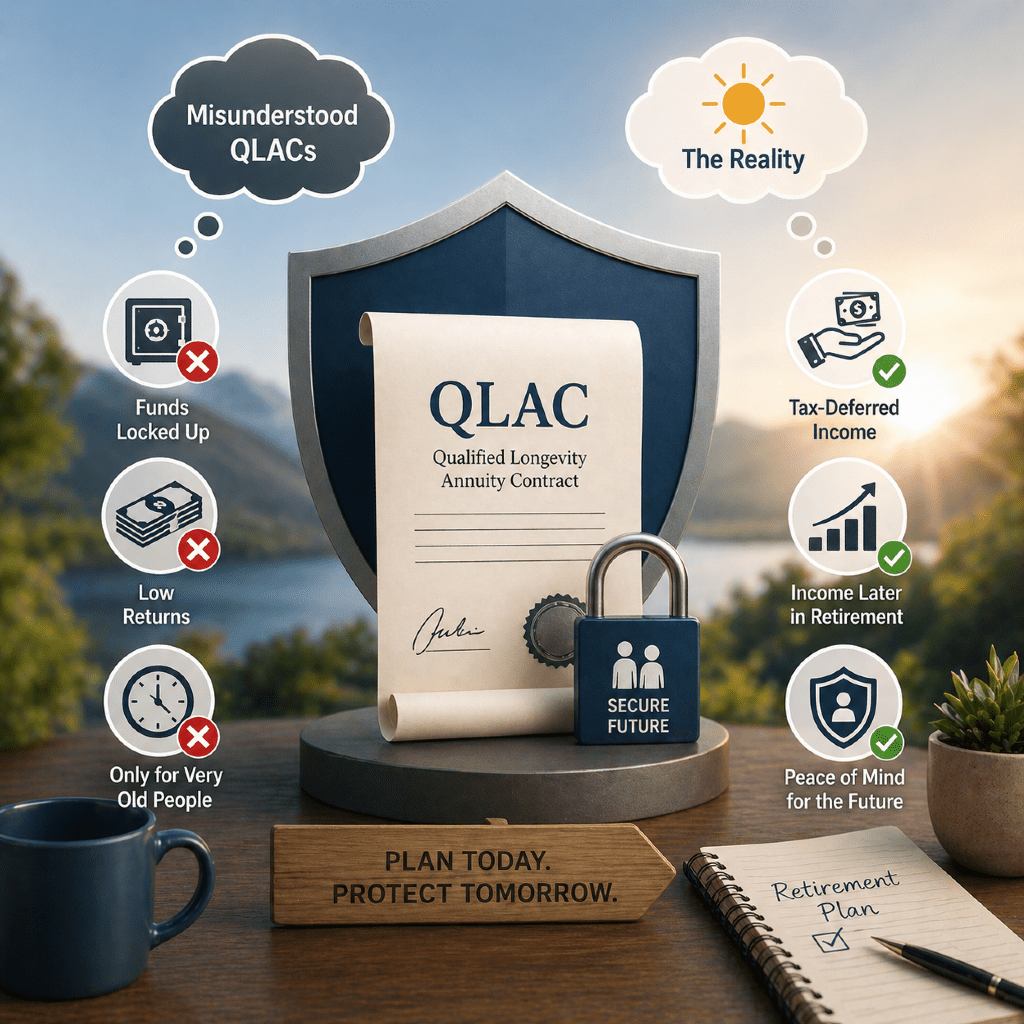

Is My Money Locked Away Forever?

Access and Liquidity Considerations

A frequent misconception is that assets used to purchase a QLAC are inaccessible in every circumstance. While QLACs are designed for deferred income, and typically do not allow for full liquidity after purchase, some contracts may permit limited features such as return-of-premium options upon death. However, once contributions are made, early withdrawals or changes are generally not permitted. Understanding these commitment terms is essential before allocating retirement funds.

Understanding Withdrawal Rules

You should recognize that QLACs operate under strict federal withdrawal guidelines. Early withdrawals (if available) can result in adverse tax consequences and may reduce the future income stream. QLACs are structured to prioritize future income stability over liquidity, meaning you should carefully balance any purchase against your broader retirement and emergency needs.

Are QLACs the Same as Other Annuities?

Key Distinctions from Other Retirement Tools

It’s a common mistake to equate QLACs with all other annuities. While both may provide guaranteed income streams, QLACs are specifically created to be funded from tax-deferred retirement accounts and to delay taxable distributions past the usual age for required minimum distributions. Traditional deferred annuities, immediate annuities, and variable annuities all have different purposes, rules, and tax treatments.

Why Misunderstandings Happen

Much of the confusion comes from the broad use of the term “annuity” to describe a wide array of products. QLACs have unique regulatory requirements, such as specific contribution limits and payout timing, that set them apart. Understanding these differentiators helps prevent mistaken assumptions about how QLACs fit into your retirement plan.

Do QLACs Eliminate Required Minimum Distributions?

How QLACs Interact with RMD Rules

QLACs offer the opportunity to defer RMDs on the portion of funds allocated to the contract, up to the limits set by the IRS. This means the amount used to purchase a QLAC is excluded from RMD calculations until payouts begin. However, all other retirement plan assets remain subject to the standard RMD rules, so QLACs do not eliminate the obligation—they simply postpone RMDs for specific assets.

Limitations and Exceptions to Be Aware Of

Deferral of RMDs only applies to funds placed inside a QLAC, up to specified contribution limits. The remaining retirement assets continue to generate RMDs according to your age and the IRS schedule. This nuance underscores the importance of understanding both what QLACs can and cannot do regarding your overall tax situation and retirement income planning.

Is Income from QLACs Tax-Free?

Tax Considerations and Timing

Another misunderstanding is believing that QLAC payouts are tax-free. In reality, income received from a QLAC is subject to ordinary income tax when paid out, since contributions usually come from pre-tax retirement accounts. The benefit QLACs provide is deferral—not exclusion from taxability. The timing of your withdrawals determines in which tax year the income must be reported.

General Tax Principles for Retirement Income

Generally, retirement income you receive from tax-deferred plans, including QLAC payouts, is taxed at your applicable ordinary income rate during the year of distribution. No favorable capital gains rates apply, and required withholding, if any, must comply with current IRS rules. Tax rules can change, and you should refer to official IRS sources or reliable tax education resources for up-to-date information about the tax treatment of QLAC-related income.

Can QLACs Solve All Longevity Planning Needs?

Balancing QLACs with Other Strategies

QLACs address the risk of outliving your retirement savings, but they should be viewed as one part of a broad retirement plan. Other strategies—such as Social Security benefits, personal savings, and various income-producing investments—also play a vital role in ensuring financial stability over the course of retirement. No single tool, including QLACs, is likely to address every need or scenario you might face later in life.

Awareness of Considerations and Limitations

It’s important to evaluate your long-term needs, preferences for liquidity, tax considerations, and the range of possible future scenarios when considering a QLAC. Understanding both their advantages and their limits—such as lack of access to principal and fixed payment structures—can prevent future disappointment and facilitate a more secure journey through retirement.